In the wake of excellent reporting about the private nature of publicly funded charter schools in Los Angeles and New Jersey, I wanted to get an answer to the question in the title of this blog post, prompted by that picture above, which I took in February.

That is: who really owns St. Coletta charter school on the far edge of Capitol Hill, at 1901 Independence Avenue SE.

Despite 96,000 pages of information on the charter board website, my unsuccessful journey to find an answer to that question, recounted below, shows that not all of those 96,000 pages are complete or transparent.

As I began my research, I found that there were three related questions that I wanted answers to in order to arrive at an answer for the question in the title of this blog post.

Thus, I asked those three other questions (which I have put below) on February 10 of both Scott Pearson, charter board executive director, and Tomeika Bowden, charter board chief communications officer.

Despite multiple promises to get back to me, I got no answers.

Of course, I could file a Freedom of Information Act (FOIA) request with the charter board. Or, more precisely, multiple FOIA requests, because what I am seeking is not likely obtainable with one request. My getting any response, however, depends on whether the charter board has this information–and the reality is, they might not. I cannot make any FOIA request of St. Coletta itself, because our charter schools are not subject to FOIA.

As you may recall, there are two pending pieces of legislation to bring about more transparency with respect to our public schools. But only one bill would ensure our DC charter schools would be responsive to FOIA like charters in 39 states. See more about it here.

The other bill, introduced weeks later, appears to have purposely avoided making our charter schools subject to FOIA.

Which is really interesting, given how much I could not find in just this one case, which I have outlined in detail below.

Indeed, given that per pupil facilities allocations for our charter schools–amounting to more than $100 million in DC taxpayer funds annually–are neither tracked nor required to be used for facilities suggests that the public is at a far remove from an answer to that question above for most, if not all, of our charter schools.

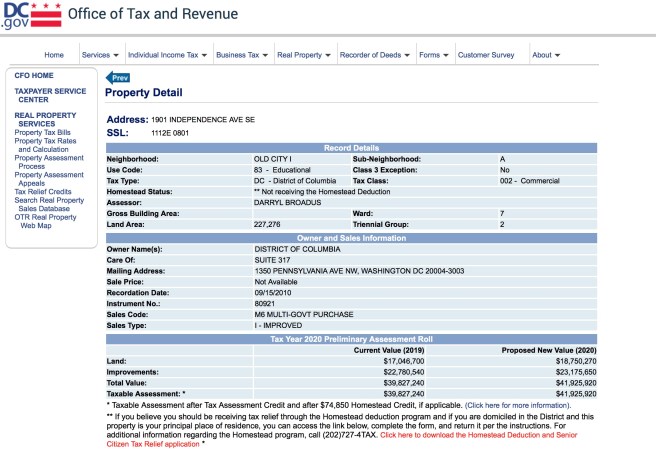

Question 1: Who owns the building occupied by St. Coletta charter school, at 1901 Independence SE?

As you can see from the screenshot below from the city’s real estate database, taken last week, DC owns the land and the “improvements” at 1901 Independence SE–which suggests the building as well as the land.

However, there is considerable muddiness in that:

The land itself was apparently leased to St. Coletta’s management company, St. Coletta of Greater Washington (SCGW), for $1 a year, for 99 years, before the current building there was built. Here’s the DC legislation that was passed regarding that arrangement.

As that legislation notes, SCGW is responsible for bearing the costs of any improvement on the land–but DC gets first dibs if SCGW decides to sell the improvements. Also, once the lease is terminated, DC gets to keep the improvements. That said, it’s not clear to me what would happen if, say, SCGW sold the improvements to an organization that is not DC, then terminated its lease.

The actual building of the St. Coletta facility at 1901 Independence SE was apparently financed by a congressional appropriation, fundraising, and DC revenue bonds. Here is the legislation for up to $16 million in DC revenue bonds to be issued for this purpose.

The building’s total cost appears to have been between $32 and $36 million. In this source, for instance, it says “the total cost came to about $32 million, which was appointed from congressional appropriations, a bond secured by Bank of America, and a capital fundraising campaign.” Another publication says a staff member noted that “a congressional earmark through the efforts of a supporting member of Congress provided one-third of the $36 million building cost. Another $6 million came from donations and the balance–$16 million–was financed commercially.” (NB: The math represented in the latter source doesn’t add up to $36 million, but $34 million.)

Interestingly, on p. 82 of the appendix to its 2015 10-year review, the school doesn’t list the building as an asset. That is in accord with St. Coletta’s most recent annual report (2017-18) as well as every single financial document for the school I was able to find on the charter board website, including in the charter board’s financial audit reviews.

But when I posed the question of who owns the building to Rebecca Hill, a St. Coletta staff member, she said that the school owns the building.

So, it appears that DC owns at least the land under the St. Coletta building, if not the improvements on the land, which would include the building itself. (To be sure, this may hinge on whether city leaders judge the city’s real estate assessment database as accurate. Recall that charter board executive director Scott Pearson disputed the database’s accuracy in the assessment of the closed WMST charter school, noting that that school’s building was assessed much too high by the city when it was sold below its assessed value (though interestingly, the WMST building’s assessed value in the database has only increased since its sale).)

The cost of building the St. Coletta facility appears to have been covered by the following: 33% federal tax dollars given outright; 50% commercial loan and/or DC revenue bonds issued for the school, either or both of which could have been paid off in part (or wholly) with annual per pupil facilities allocations from DC taxpayers; and 17% donations.

It thus appears that the majority of the funds paying for the building itself were public, with the public owning at least the land underneath the building.

To be sure, St. Coletta is hardly alone in this murky mixing of private and public in DC charter school real estate.

For instance, both DC Rocketship charter schools were built on land purchased by LLCs based in California, associated with the Turner Agassi charter organization. In each case, I could not find how much public money (if any) was used to build the schools in each location (see here for a recent press release). Regardless, each year Rocketship pays out facilities fees to use both schools (for the current school year, more than $5 million). Purchased for about $5 million several years ago, the two properties are now together assessed at nearly $40 million. In the fall, the council approved $30 million in revenue bonds for a Rocketship entity to buy out its lease at one of the schools. Thus, whatever transpires, the private owners will likely profit considerably by leveraging the purchasing power of public money, in the form of DC’s per pupil facilities allocations.

Question 2: What amount of per pupil facilities payments has St. Coletta and/or SCGW received by year since St. Coletta started in DC as a charter school?

In looking at the financial statements of St. Coletta available in the appendix of its last review in 2015, for most years there are no per pupil facilities allocations mentioned (see for instance, the “unaudited year-end financial statements for 2013-14” (p. 34) as well as that document for 2014-15 (p. 80) and the auditor’s statement for the years ended June 30, 2011 and 2010 (p. 162)).

[Ed. Note: to access these page numbers for easier searching, export the file from the link above as a PDF.]

That said, in an auditor’s report (on p. 196 of the appendix of its last review), there is $750,000 listed for 2014 and $750,000 for 2013 for facilities allocations from the city. Those amounts make sense to me, because the school has about 250 students, and at $3,000 per student for facilities allocations to DC charter schools, that comes out to $750,000 per year.

That figure also appears in accord with the school’s most recent annual report, which shows that for 2017 the school’s DC per pupil facilities allocation was $788,000.

Where the rest of the school’s annual facilities allocations are listed or accounted for, however, is not obvious to me.

Prior years’ annual reports are not available on line on the webpage with annual reports, though there are financial analyses from 2012 on available online that do not appear to have the annual facilities allotments separated out from other DC funding allocations. Even in the 3-years-running tax records (990 forms) available online, I found that it appeared to be school-dependent whether per pupil facilities allocations were separated out from other per pupil allocations from the city.

The documents I saw on those web pages showed what appeared to be increasing assets for the school over recent years (i.e., in June 2015, it had less than $1 million in assets, and in June 2018 it had $3.4 million). But how those assets increased, and what they specifically consist of, remain unclear to me. (Recall that DC doesn’t require charter schools to use per pupil facilities allocations for facilities–and there is no public tracking of how the >$100 million in annual facilities payments given to DC charter schools are used.)

Thus, the only thing that appears clear to me is that my not being able to get an answer to this question is hardly unique to St. Coletta.

Absent voluntary reporting of annual facilities allocations by each DC charter school; the power of FOIA over those schools; and/or mandated tracking of facilities funds, DC taxpayers have no idea of the totality of facilities allocations granted to any one school; what those funds are/were used for; and the relationship of those facilities allocations to any growth in assets.

Question 3: Did anything happen with respect to the charter board’s recommendations in its 2015 review to disaggregate the school’s finances from those of its management company, SCGW?

The revenue bond legislation for St. Coletta provided for the bonds to be issued to both the charter school as well as SCGW–which to me considerably muddies the picture of who (or what) actually owns this school or its building (or both).

The charter board also has been confused–and apparently concerned.

For instance, in a statement from p. 17 of the school’s 10-year review from 2015, the charter board said this:

“If St. Coletta PCS were to cease operation for any reason, it would be difficult to determine what remaining public funds and physical property should be returned to the District of Columbia, because the school’s finances are integrated with those of the non-profit [SCGW].”

In that review, the charter board makes clear its discomfort with the fact that all money seemed to flow through SCGW to St. Coletta. It thus recommended the following (from p. 3 of the 2015 review):

“Segregation of the School’s Financial Statements. The school and its management company should revise the format of their financial statements to separate the school from the other parts of the organization. This will enable DC PCSB [the DC charter board] to effectively monitor the school’s financial stability and verify the use public funds.

“Compliance with Procurement Contract Submission Policy. The school has not submitted any documentation regarding procurement contracts to DC PCSB. To demonstrate compliance with the SRA’s [school reform act] requirements in this area, St. Coletta PCS should submit all procurement contract documents – including solicitations, bids received, executed contracts, and the determinations and findings form – to DC PCSB for the current fiscal year (FY16) and all future years.

“Transparent Reporting of the Management Fee. Currently, the difference between the school’s revenues and expenses are retained by SCGW as its management fee. The school should report the management fee separately from all expenditures related to the school’s operations.”

When I tried to see whether the charter board had subsequently voted on or made any changes or comments with respect to St. Coletta’s accounting, I got no search results when I searched the board meeting part of the PCSB website.

I also got only the following 4 items when I searched items open for comment on the charter board website using as my search term “coletta”:

–Notice of petition to amend charter: goals and academic achievement expectations, with a vote date of 1/22/18

–Notice of petition to amend charter: special education enrollment preference, with a vote date of 9/18/17

–Notice of petition to waive special education LEA status requirements, with a vote date of 7/17/17

–Notice of petition to amend charter, with a vote date of 12/15/14

Moreover, none of the links worked for the first two items–and none of the items seem to concern themselves with the issues raised above regarding accounting between SCGW and St. Coletta. (I was able to backtrack through board meeting recaps to see what was actually voted on for those 4 items. None seemed to be concerned with the building or SCGW’s finances.)

Potentially confusing matters, in the most recent financial analysis review on the charter board website (from 2017, available here), there is a note in the St. Coletta financial report card (available here) that says this:

“For 2017 and 2016, 100% of the school’s expenses were paid to SCGW as management fees amounting to $17.8M and $17.3M, respectively. Because the school’s revenues net out against the management fees paid to SCGW, certain financial performance metrics are not applicable, e.g., the school has no debt or other obligations and over 95% of liabilities consisted of payments to SCGW.”

In the 2016 financial audit review, there is a note in the financial report card for St. Coletta that says this:

“St. Coletta of Greater Washington, Inc. (SCGW) provides facilities, equipment, personnel, financial management, operating services, and supplies to the School. The School pays SCGW a fee equal to the revenue and support of the School. In 2016, the School paid SCGW a fee for management services of $17.2M. Please note that the highest paid employee above was taken from the most recent 990 available at the time this report was produced. To access the Consolidated Financial Statements of SCGW for the year ending June 30, 2016, please use the following link:

https://www.stcoletta.org/downloads/AuditedFinancialStatements_63016.pdf”

Not only does that link not work, but those two recent financial documents available on the charter board website (the 2017 financial analysis review and the 2016 financial audit review) suggest that there has been little, if any, financial disaggregation between SCGW and St. Coletta since the charter board recommended that action in 2015–and no clear way to access financial statements for SCGW itself.

(As far as the charter board’s concern with contracts goes, the charter board’s record of them on its website is completely disaggregated, so one cannot search for any one school–only by month. I looked at the records for 2018, and it appears that the school is reporting its contracts–but each one I saw seemed to have some trouble with being reported on time or completely.)

All of which is to say that I appear to not have an answer to the question in the title of this blog post–and have to wonder what the council was thinking in promoting legislation that will not help whatsoever to answer it.

One thought on “Just Tell Me: Who Owns This?”