This week, a coalition of education advocates demanded a public hearing around the collapse of Eagle Academy.

Sadly, they have ample reason for that demand.

Consider that on August 23, Phil Mendelson, the chair of the DC council (i.e. pretty much the only person exercising any education oversight in the Wilson Building), sent a letter with questions about what happened at Eagle Academy to the charter board. A few weeks later, on September 9, the charter board produced this in response.

While there remain many unanswered (and unasked!) questions around Eagle, this September 9 charter board response document bears a closer look, as its obfuscation and misrepresentation go in many directions.

Indeed, the charter board’s 9/9/24 response document shows that

–fiscal opacity around DC charters is designed to advantage LEAs over the public in general and LEA families in particular;

–that opacity originates with the charter board’s fiscal oversight processes, which are not robust; independent; or sufficiently publicly centered either to prevent what happened with Eagle OR to protect LEA families; and

–the problems those things create and ultimately encourage are not limited to Eagle. (Here, for example, is what happened recently with KIPP DC; despite huge differences between these LEAs, the common denominator is that charter board processes did not prevent fiscal mismanagement and excluded the public while advantaging the LEAs.)

To outline specific problems in the charter board’s 9/9/24 response about Eagle, I emailed the council chair and committee of the whole staff the 14 items below. Since sending my missive out on 9/11/24, I have gotten silence from the council—and also learned that the charter board response document is silent on two important issues:

1. DC resident Camille Joyner pointed out that this September 9 charter board response document weirdly avoids all mention of 2016—a significant year fiscally for Eagle.

That year, Eagle’s cash on hand dropped significantly, while the LEA purchased the property at 2345 R SE in August 2016. Then, starting in October 2016 and going through July 2018, two Eagle staff members–CEO Joe Smith and someone who is unidentified–loaned the school >$600,000. While this was outlined in financial documents posted by the charter board, it was entirely unmentioned in this September 9 response. Such loans are considered self-dealing and prohibited by the IRS.

Also in 2016, Cassandra Pinkney–the co-founder and co-leader of Eagle with its CEO Joe Smith–died. As Ms. Pinkney was apparently ill before her death in September of that year, Joe Smith was possibly the only source of the LEA’s 2016 fiscal issues.

2. Eagle CEO Joe Smith was also the head of the charter management organization (CMO) that, starting in 2020, had a close relationship with Eagle outposts in Nevada and Ohio. Yet the September 9 charter board response document entirely avoids any mention of the extensive connections of DC personnel (and possibly finances) to those other Eagle schools.

Now, we wait for DC to act on any of this.

Consider that after just 1 year of Eagle’s operations there, Nevada officials managed to hold multiple hearings about the school’s fiscal adventures—and wasted no time in shutting it down.

By contrast, the DC charter board had its first public hearing about Eagle’s fiscal issues in July, almost a year after it began monitoring the LEA’s finances. The next month, the charter board voted to not approve Friendship taking over, which Eagle had wanted. Despite Eagle’s apparently intractable fiscal problems, the charter board never voted to rescind Eagle’s charter–unlike what the Nevada board did. Instead, the DC charter board’s August vote prioritized Eagle’s specific ask over the more pertinent (and ultimately more pressing) interests of families and taxpayers.

It remains to be seen now if DC’s years of poor oversight of its charters; unasked and unanswered questions around Eagle; and the charter board obfuscations outlined below will even merit a DC council hearing.

————————————————————————————————————-

Problems With The DC Charter Board’s September 9 Response To Chairman Mendelson’s Questions

1. Early in this response document (on p. 2), it says that “a memo is read into the public record at a public Board meeting following each Finance Committee meeting that lists the LEAs on the Monitoring List, as well as LEAs now subject to a Financial Corrective Action plan (FCAP).”

AFAIK there are no publicly noticed meetings of the charter board’s finance committee, so the public will not know when they met nor when their decisions would be read into the record. In addition, there appears to be no listing of those readings into the record anywhere except in the specific board meeting where they were read into—and no way to search for them on the charter board website.

The same appears to be true for fiscal notices of concern and fiscal out of compliance notices. In fact, when I asked the charter board (PCSB) for a copy of the fiscal out of compliance notice issued for Eagle in January 2024 (as mentioned at the July 10 board meeting), I was initially told that it was an internal document and not available to the public. After weeks of me inquiring, the charter board finally posted it publicly in August. (See the email chain here: https://drive.google.com/file/d/1Xg5nJxMrjnWZ2yOL-2uRoPTpJLOoejY5/view?usp=sharing)

Unfortunately, what the charter board posted in August had different dates than what was reported at the 7/10/24 board meeting and included TWO documents issued to Eagle in January 2024 (see here https://dcpcsb.egnyte.com/dl/GQva5VfAce and see here https://dcpcsb.egnyte.com/dl/F0QrhUKvRQ).

As a result, the charter board corrected its 7/10/24 hearing memo weeks after that board meeting (see footnote 3 on p. 4 of that memo here: https://dcpcsb.egnyte.com/dl/hDQvAiaA9S).

Bottom line:

Because there appears to be no way to search for these items (and AFAIK they are not listed on PCSB annual reports—which are not timely anyway) and no way to know when FCAPs or memos or notes about fiscal monitoring are read into the record, this is public information that is essentially unavailable to the public. Requesting this information by FOIA is not a solution because it’s not timely and the public has a right to access it in a timely manner.

2. On p. 4, the response document says that in June 2023, Eagle was placed on DC PCSB’s financial Monitoring List.

But this financial monitoring list is not publicly available anywhere that I can find. This again is meaningful information that the public has no access to in a timely manner.

3. There was no mention of important items on p. 2 of the response document in the January 2023 20-year review of Eagle (https://www.livebinders.com/media/get/MjM4OTMzNTQ=), such as

—October 2022 fiscal monitoring of Eagle by PCSB

—The fact that Eagle was on the fiscal monitoring list in November 2019

—The fact that Eagle was removed from fiscal monitoring in May 2021

And both the January 2023 20-year review and this response document omit entirely what was going on in 2021, which was the creation of Eagle charter schools in Nevada and Ohio that not only had overlaps with DC personnel (Joe Smith, Jai (Julinda) Mallory, and Scott Knowlton), but also had the same CMO with Joe Smith at its head, for which Eagle DC personnel and techniques were key.

4. On p. 4 of the response document, there is this note for September 2023:

“With the school’s ample working capital and current ratio, the increase in days of cash on hand, and FY 2024 budgeted financial indicators above DC PCSB targets, it would have been premature to require a financial corrective action plan (FCAP) at that time.”

This statement appears to directly contradict what a staffer for Eagle testified about at the July 10, 2024 hearing, where she said Eagle became aware of fiscal problems and the need for financial correction in October 2023. (See pp. 63-4 of the 7/10/24 transcript, where the staff member notes that the school’s budget began to “shift” in October 2023, such that the school had its first round of staff cuts in December 2023. The 7/10/24 meeting transcript is here: https://dcpcsb.egnyte.com/dl/iLmlTvhznf)

Even if we assume that this staffer was not telling the truth on 7/10/24, the reality is that PCSB’s assumptions here—that all seemed OK with Eagle’s finances in September 2023—were clearly wrong, as we know what happened shortly thereafter.

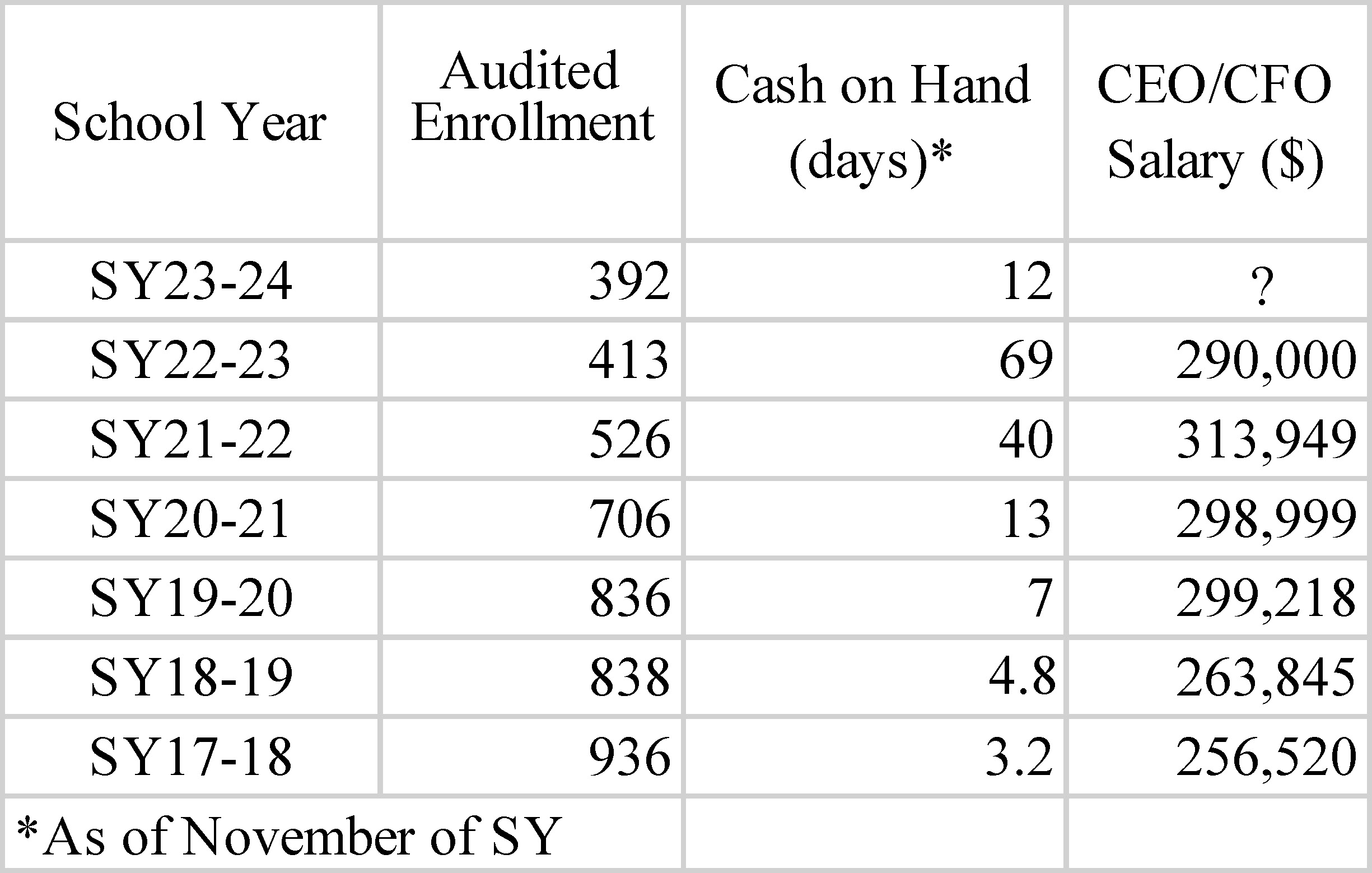

5. There also appears to be no mention in the response document of the actual (low) days of cash on hand for years running, alongside the declining enrollment and the high salary of Joe Smith. Here is what that looks like:

(Data here is from the charter board’s financial analysis reports (cash on hand); audited enrollments; and 990s and the SY22-23 Eagle annual report (salary).)

6. On p. 4 of the response document, it says this (boldface mine):

“We did not propose an FCAP on January 17, 2024 at our FY 2024 Q1 Finance Committee meeting because we had not yet received the FY 2023 audited financial statements that revealed more concerning issues. At the time of the Q1 review, the school’s working capital was healthy, and forecasted days of cash at year-end for FY 2024 were above target.”

Yet on p. 2 of the board memo for the July 10 board meeting (https://dcpcsb.egnyte.com/dl/hDQvAiaA9S) it says that “the school’s audited financial statements, issued on January 18, 2024, reflected 23 days of cash on hand as of fiscal year end (FYE) 2023, below the 30-day floor for this measure.”

Regardless of how one views “23 days of cash on hand” (i.e. “healthy working capital” or not good at all), we know that no one at the charter board until 1/18/24 had an audited financial statement to give a more timely picture of the school’s finances.

But unlike this response document, the board memo for 7/10/24 goes into much more detail as to what the charter board was seeing immediately after January 18, 2024—and it was NOT good by any measure!

Take this passage, from p. 5 of the July 10 board memo:

“As the school’s liquidity had deteriorated significantly as of February 29, 2024, per monthly financial statements submitted by the school on March 30, 2024, DC PCSB requested the school provide a third revised budget forecast projections for FY 2024 and the preliminary budget for FY 2025. The provided budgets were subsequently adjusted several times as the school responded to questions about its economic viability through the July UPSFF payment.”

Unlike this response document, that 7/10/24 board memo passage above suggests that immediate action needed to be taken by the end of MARCH if Eagle was going to have any chance to survive for SY24-25 (i.e. through the July UPSFF payment). Yet no FCAP was assigned UNTIL July—and this response document appears to justify that delay.

7. The response document says this on p. 6:

“During the week of July 1, Eagle Academy PCS’s board informed us they were in talks with two or more LEAs that were interested in acquiring the school. The option that gained most traction was an acquisition by Friendship PCS. The schools began negotiating an asset acquisition agreement, which would address the transfer of assets and liabilities from Eagle Academy PCS to Friendship PCS and guarantee the enrollment of every current Eagle student. Friendship PCS’s board voted to extend an offer to acquire Eagle Academy PCS at their board meeting on July 12. Eagle Academy PCS’s board approved the proposal on July 18. We made it clear to both LEAs throughout the process that DC PCSB’s Board would have to approve the request for it to proceed.”

Nowhere is it stated that this plan was completely unviable out the gate.

For one, the lease for McGogney, one of Eagle’s facilities, specifies that DGS has to approve any new tenant first. That was not done by that point.

For another, even if just a portion of McGogney was sublet, the lease specifies a 30-day notice period to DGS for that purpose. But by the time this takeover was approved by Friendship and Eagle, it would have been too late for DGS to have met that 30-day notice period before the start of school.

So despite the votes by the LEA boards, and PCSB knowledge of those votes, NO ONE in any of these bodies had anything to do with DGS on this subject NOR had any right to change lease terms for that facility in the desired time frame.

As it is, the idea that Friendship—and only Friendship!—was best suited for this role is absurd. There was no vetting by anyone except Eagle—which meant that whatever deal Eagle worked out was necessarily best suited for the two private entities involved, not necessarily (or ever) for DC and Eagle families.

And while the charter board itself could have played a role in all of this, it obviously chose to abrogate its responsibility, allowing the private interests of two LEAs to trump those of Eagle families and DC taxpayers.

8. On p. 7 the response document says this about what was happening in August 2024:

“Certain items were definitive about Eagle Academy PCS’s financial position. Others remained variable; the variability is important to note because each decision made could move the mark forward or backward substantively enough for the school to meet or miss its corrective action plan targets or Fiscal-Year-End cash requirements.”

These sentences are very misleading because by August, if ANY school or LEA doesn’t have a solid financial footing in any reasonable and expected scenario, that LEA cannot function appropriately for the coming school year period.

A solid financial footing was not the case here in August—by the charter board’s own statement that “each decision [of Eagle] could move the mark forward or backward substantively”!

This suggests, again, that Eagle was allowed by the charter board to do what it wanted when it wanted, while the responsibility that the charter board could have exercised—say, to institute the FCAP in January and then revocation by late spring if no improvement—was abrogated at multiple turns.

9. On p. 8 of the response document it says this:

“For some public charter schools, budgets are often tight and resources are limited in providing optimal segregation of duties. In such cases, some of the CFO responsibilities are outsourced to work cohesively with the CEO and serve as another pair of eyes. . . .After receipt of the FY 2023 audited financials and as DC PCSB dug deeper into the root causes for the school’s financial problems, it became clear that Joe Smith had been struggling with his roles. The school’s board acknowledged publicly it had planned over a year ago to split the roles but failed to take the appropriate actions until June 2024.”

This is very misleading:

—For one, while Joe Smith may have been “struggling with his roles” as both CFO and CEO, the reality remained that the charter board was OK with years of repeated low cash on hand at this LEA while Smith himself received outsized salaries, even as the enrollment dropped precipitously (see the table in #5 above).

—For another, Smith starting in 2021 was the head of a CMO he created through Eagle Academy to branch out into Nevada and Ohio. Thus, if he was “struggling with his roles,” he was also enriching himself in that struggle, something that the charter board has never publicly acknowledged AFAIK.

—And for yet another, the idea that a small LEA might combine a CEO and CFO role due to lack of funding is misplaced here. It behooves the charter board to ensure there is adequate fiscal oversight AT the LEA itself regardless of who is at its head. But among other things, the July 10, 2024 hearing made clear there was NO adequate fiscal oversight at Eagle—while PCSB itself, knowing this for years per this response document, provided no backstop.

Here, for example, is what the acting head of school said (from p. 63 of the July 10, 2024 meeting transcript, boldface mine):

“The culture at Eagle was not a collaborative culture. So, the budget, and the finances, those meetings were closed meetings that were held between the CEO/CFO and the accounting team. That’s pretty much the financial team. So, senior staff, heads of departments, we were never part of the process. We were not in the decision making meetings, we were not kept abreast, and whatever was presented at for example board meetings, was what they determined to present, and it made it seem we were relatively stable. We were actually told we were in a good financial position until around about October it slowly started to shift.”

10. On p. 8, the response document says this:

“Joe Smith’s dual role as CEO and CFO did not on its own raise a red flag. The school’s auditor, which served in that capacity each fiscal year since at least FY 2014, did not cite as an internal control weakness the lack of segregation of duties in any of its audit reports.”

This statement displays an unwarranted trust in those audit reports, which are done by auditors selected and paid for by the LEAs themselves.

This by itself doesn’t mean that the auditors are not doing their jobs!

But it does mean that there is a lack of independence in those audits, inasmuch as the hired auditors look at only what is given to them by the LEA. This closed system is not good for fiscal transparency or the public interest—and there is no backstop to it by the charter board.

11. On p. 9, the response document says this:

“DC PCSB reports the issues in the school’s financial report card in its annual Financial Analysis Report (FAR), including unresolved prior year findings.”

This is not true for Eagle. For instance, on the most recent FAR (https://dcpcsb.egnyte.com/dl/9rv9ElIrHO/FY_2022_Financial_Analysis_Report.pdf_ which was posted in October 2023, for FY22), it says the following for Eagle on p. 85: “We will continue to closely monitor the LEA’s financial position to ensure it maintains sufficient liquidity.”

There is NOTHING said here about the fiscal monitoring in October 2022 that this response document says on p. 2 was instituted for Eagle.

Likewise, neither the FY21 FAR report (https://dcpcsb.egnyte.com/dl/Tm1JvmtBeN/FY_2021_Financial_Analysis_Report_(FAR).pdf_ posted in October 2022) nor the FY20 FAR report

(https://dcpcsb.egnyte.com/dl/XwUqqyAsEa/DCPCSB_FAR_Report_FY20_Final.pdf_ posted in October 2021) say anything in their write-ups of Eagle about the May 2021 release from monitoring mentioned on p. 2 of this response document.

And the FY19 FAR report (https://dcpcsb.egnyte.com/dl/biu7bUGJby posted in October 2020) says NOTHING about the November 2019 fiscal monitoring mentioned on p. 2 of this response document.

In fact, I could find on none of the FARs any clear record for notice of fiscal concerns, monitoring, or other financial flags of the charter board for the reported time periods.

This seems like a real public oversight that can easily be resolved by keeping public tabs of all such monitoring.

12. On p. 10 the response document says

“Historically during those [5-year] reviews, we have not looked at the LEA’s work outside the District. We are working with the DC PCSB Board to strengthen our reviews and intend to include the out-of-state activity in those going forward. Eagle Charter School in Nevada, was governed by a different nonprofit than the DC LEA. . . . Nevada’s actions to address financial and enrollment issues at a school operated by a different nonprofit did not play a role in our oversight.”

There are several things to unpack here:

—While it is true that Eagle Academy was a nonprofit here in DC, legally separate from the Eagle CMO (Eagle Charter Schools Inc, or ECS) behind both its Nevada and Ohio branches, it is also true that ECS was closely associated with DC’s Eagle Academy. For one, the same person, Joe Smith, headed both. For another, ECS depended on DC’s Eagle Academy staff and processes. And for yet another, the personnel heading those Nevada and Ohio operations (Jai (Julinda) Mallory and Scott Knowlton, respectively) were right-hand employees of Joe Smith here in DC, including working at both places at the same time.

Thus, although the separation of these nonprofits is clear, there are nonetheless considerable connections.

—Eagle is not the only DC charter to have operations in another jurisdiction under another nonprofit. Friendship has other branches elsewhere and the last I knew, all of them are headed by Donald Hense. Rocketship, too, has other branches as well as BASIS and St. Coletta. I have not investigated the connections between the DC branches and those other LEAs elsewhere—but it is well worth the inquiry, given the dozens of millions DC taxpayers annually invest in just those few LEAs here.

13. In response to question 7, about the January 2023 20-year review for Eagle, the response document says that the fiscal health of the LEA was “in reasonably good shape until after the review period window.”

That is belied by the chart in #5 above.

And as noted in #3 above, the January 2023 20-year review of Eagle (https://www.livebinders.com/media/get/MjM4OTMzNTQ=) says nothing about

—The October 2022 fiscal monitoring

—The fact that Eagle was on the fiscal monitoring list in November 2019

—The fact that Eagle was removed from fiscal monitoring in May 2021

The January 2023 20-year review also omits what was going on in 2021, which was the creation of Eagle schools in Nevada and Ohio that not only had overlaps with DC personnel but also had the same CMO, for which Eagle DC personnel and techniques were key.

14. The subtext of the answer to question #8 (on p. 11) of the response document is that the July 2024 notification to families about fiscal problems at Eagle was standard, if not acceptable.

But the charter board itself knew of serious problems well before July 2024 and never directly notified the public about them, whether through making monitoring lists, notices of fiscal concern, or other documents clearly and obviously available TO the public or simply notifying Eagle families of them.

By doing that, the charter board allowed the LEA to set its own notification policy—which was directly in the LEA’s interests, as Eagle would likely have lost even more enrollment once its fiscal troubles were made widely known.